Agya mint a beretva, de a beszédén nagyon érződik, hogy mennyire megöregedett

Agya mint a beretva, de a beszédén nagyon érződik, hogy mennyire megöregedett

"Berkshire Hathaway egy 6,8 milliárd dolláros készpénzes ügylet keretében felvásárolja a Taylor Morrison lakásépítő vállalatot. Ez az új vezérigazgató, Greg Abel irányítása alatt kötött egyik első jelentős tranzakció, amely az amerikai lakáspiac hosszú távú fellendülésére tett stratégiai lépésként értelmezhető"

https://www.portfolio.hu/ingatlan/20260603/dontott...

Hát ez ennyi volt :(((

"My Fellow Shareholders:

I will no longer be writing Berkshire’s annual report or talking endlessly at the annualmeeting. As the British would say, I’m “going quiet.”"

https://berkshirehathaway.com/news/nov1025.pdf

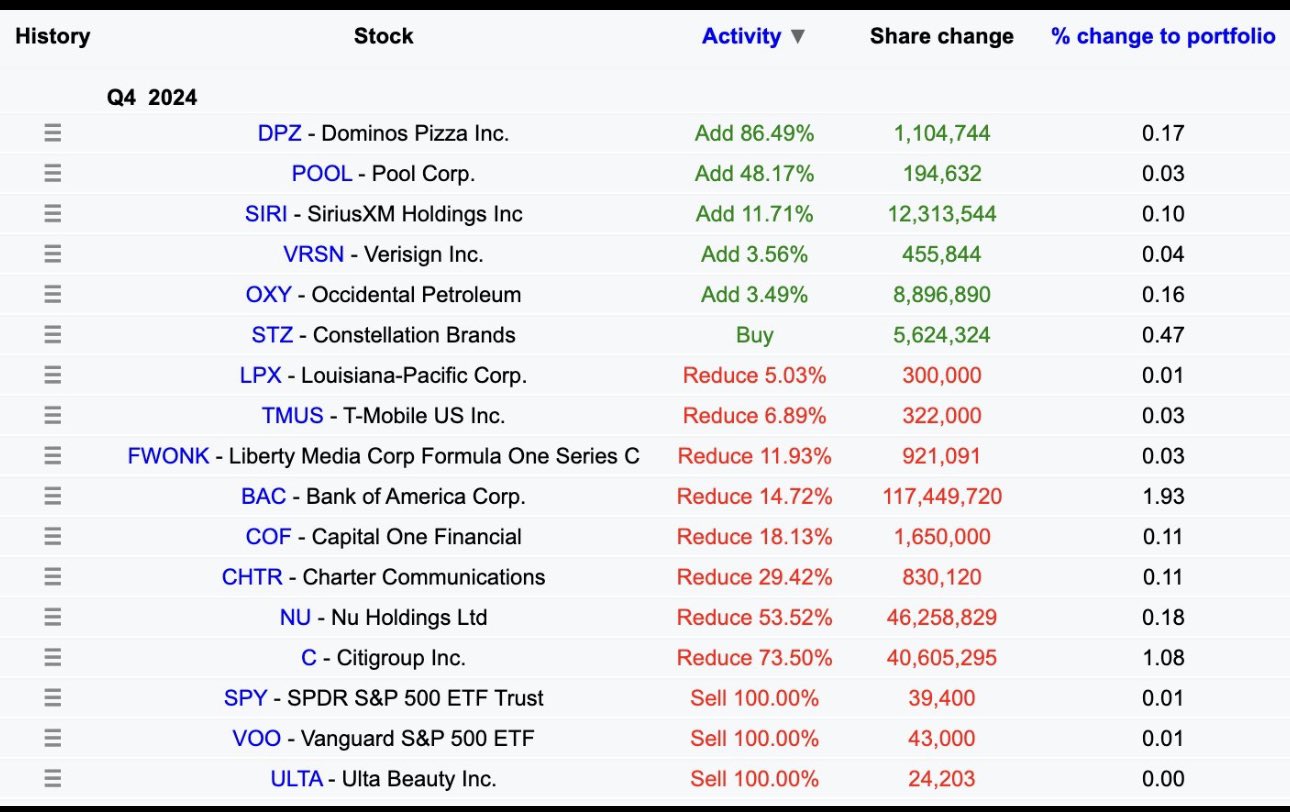

Inkább mit csinált 22-ig? Eladott, mint vásárolt..

Apple volt nagy fogás, BYD, TSMC, de ezeket leépítette.. ezt követően minimális vásárlás volt, inkább eladott..

A cash amcsi állampapírba van..

Most lesz izgi, hogy az utód mit fog csinálni?

nagyot varázsolt az öreg 2022 után.

Nvidia, vagy FB , vagy mibe pakolt ennyi lóvét?

"Buffett az év végén lemond a Berkshire vezérigazgatói posztjáról,

és a hat évtizede épített vállalat irányítását a 63 éves Abelre bízza, miközben elnökként a helyén marad.

A májusi éves közgyűlésen sem válaszol majd a befektetők kérdéseire – ez eddig a rendezvény egyik fő eleme volt, amely évről évre ezreket vonz a Nebraska állambeli Omahába. A színpadon helyette Abel lép fel."

pizza, medenszié, pia, rádió, olaj, internet... kell ennél több? :))

ezen én is gondolkodtam. Egy szaros rádiót üzemeltető cég. Ez olyan ódivatú jövőtlen dolog manapság.

Mai közzététel: https://www.berkshirehathaway.com/news/nov2524.pdf

Remélem jól van az öreg.

Lehet érez valamit, hogy jöhet valami pityputy...

Warren

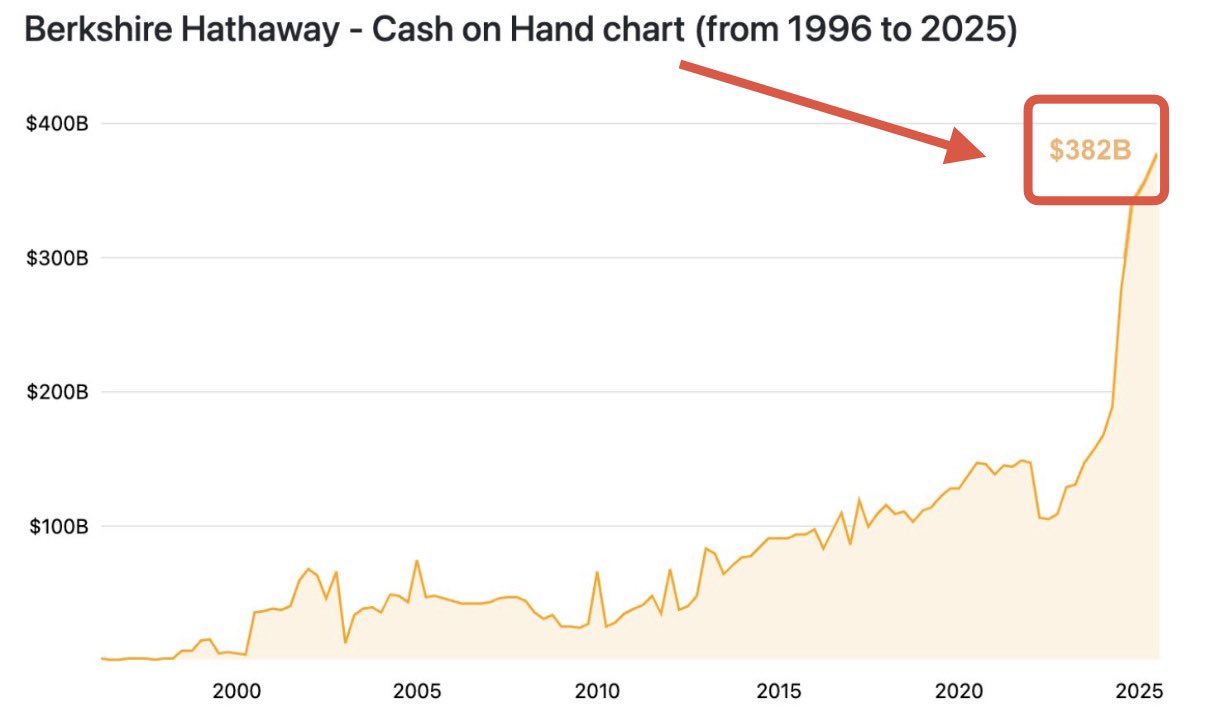

Buffett cége megvehetné az összes NFL-csapatot – így indul a Visual

Capitalist cikke, amely a Berkshire Hathaway készpénzállományáról szól.

Ugyanis azzal, hogy az idei harmadik negyedévben a Berkshire 36 milliárd

dollárnyi részvénytől vált meg, a készpénzállománya 325 milliárd dollár

fölé nőtt. Ez bő másfélszer nagyobb, mint a teljes, nagyjából 202

milliárd dolláros magyar GDP.

A Berkshire már jó ideje szórja ki a részvényeket (különösen az Apple-

és Bank of America-papírokat), és nem is igazán vesz újakat helyettük.

Az előző negyedévet még 276 milliárd dollárral zárták. Sőt, a vállalat a

sajátrészvény-

Amcsi állampapír

https://markets.businessinsider.com/news/bonds/war...

"The company held $234.6 billion in short-term US Treasury Bills at the end of the second quarter..."

"It also eclipses the Federal Reserve's T-bill holdings, which stood at $195.3 billion as of last week"

"For context, the 1-month T-Bill yields 5.33%, the 3-month T-Bill at 5.22%, and the 6-month T-Bill at 4.95%.

Those

interest rates should generate risk-free gains of about $12 billion

annually for Berkshire Hathaway's massive T-Bill holdings, or quarterly

gains of about $3 billion."